MATH 563 — Mathematical Statistics

Hypothesis Testing

Casella & Berger Ch. 8

Assignment 4 due 3/13

Assignment 5 due 4/10

Fred J. Hickernell

May 19, 2026

Hypothesis Testing Framework

(CB §8.1–8.3; WMS §10.1–10.2)

Null hypothesis \(H_0\) — the default assumption, often of the form \(H_0: \theta = \theta_0\) or \(H_0: \theta \in \ct_0\)

- innocence, “no effect” or “status quo”

Alternative hypothesis \(H_A\) — the alternative, often of the form \(H_A: \theta = \theta_1\) or \(H_A: \theta \in \ct_A\)

- guilt, “effect”, or “change”

Test statistic \(T(\vX) = T_n(\vX) \in \ct\) — a function/summary of the data, \(\vX = (X_1, \ldots, X_n)\), used to assess \(H_0\)

Rejection region \(\RR \subseteq \ct\) — values of \(T(\vX)\) for which we reject \(H_0\)

Decision rule — reject \(H_0\) if \(T(\vX) \in \RR\)

Type I error \(\alpha\) — reasonable doubt, probability of falsely rejecting \(H_0\)

- \(H_0\) gets protection via the bound on Type I error

\(p\)-value — (under \(H_0\)) probability that the test statistic is at least as extreme as the observed value

Type II error \(\beta\) — probability of failing to reject \(H_0\) when \(H_A\) is true

Power \(1-\beta\) — probability of correctly rejecting \(H_0\)

Hypothesis testing is a formal way of deciding whether the data provide enough evidence to overturn a protected default assumption

We will use ideas from estimation, confidence intervals, and pivots

Example: Server Reliability Claim (Mean Time Between Failures)

Suppose

\[ X_1,\dots,X_n \IIDsim \Exp(1/\mu), \qquad \Ex(X)=\mu \]

Here

\(X_i\) is the time between unexpected server failures (e.g., crashes/outages) for a particular service

The provider claims the mean time between failures is \(\mu_0 = 200\) hours

We want evidence that reliability has worsened, i.e. failures are happening more frequently

Step 1: Hypotheses

- Null hypothesis (innocence, status quo): \(\qquad H_0:\ \mu=200\)

- Alternative hypothesis (guilty, change): \(\qquad H_A:\ \mu<200\)

Step 2: Construct test statistic

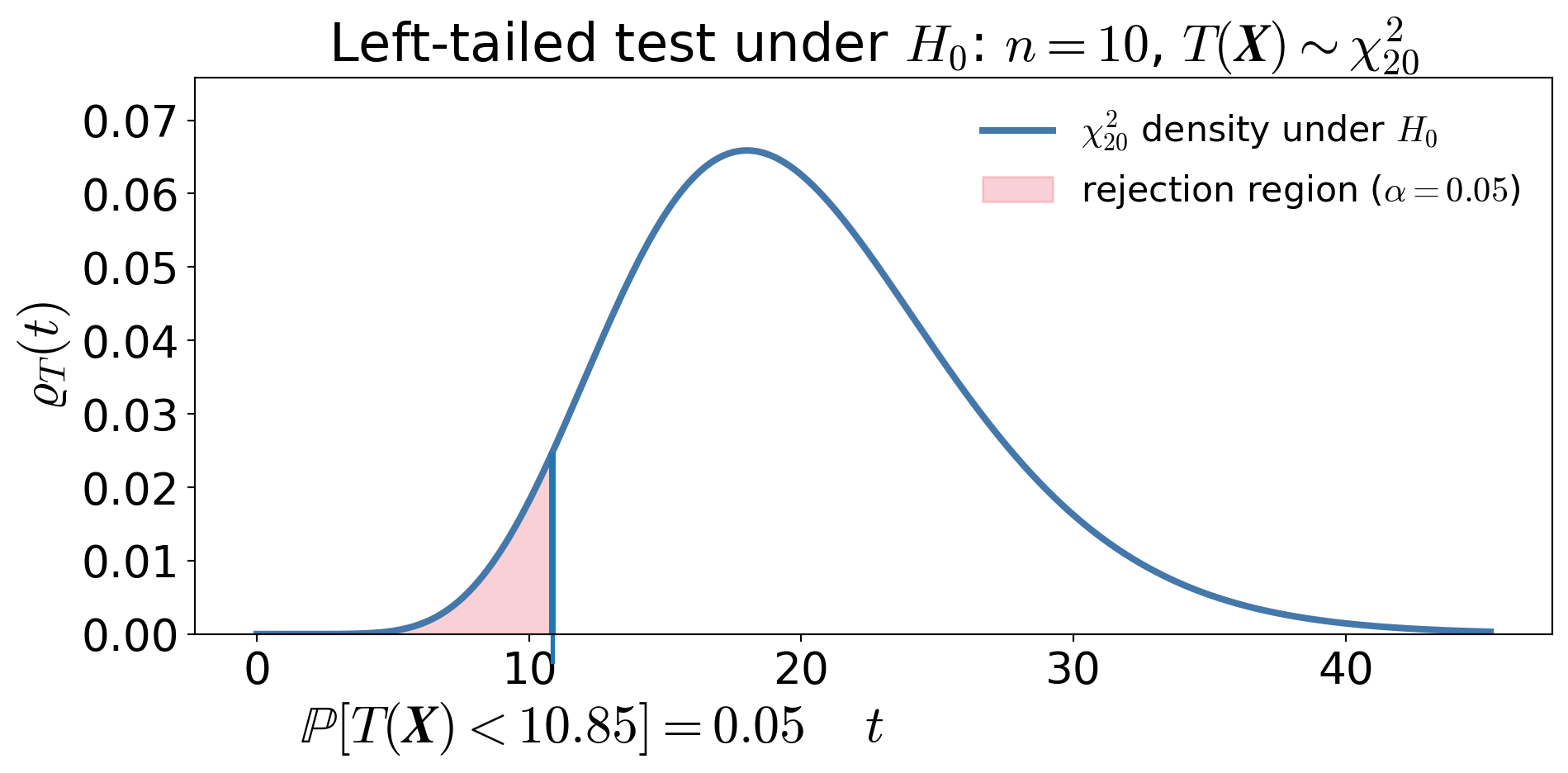

\[\text{Use the pivot } \frac{2n\barX_n}{\mu} \sim \chi^2_{2n}, \qquad \text{so that under } H_0: \mu = 200, \quad T(\vX) = \frac{2n\barX_n}{200} \sim \chi^2_{2n}\]

Step 3: Choose significance level and construct rejection region

Choose \(\alpha = 0.05\) as the maximum tolerable risk of falsely accusing underperformance

Left-tailed test:

\[\RR = [0, \chi^2_{2n,1-\alpha}) = [0, 10.85)\]

Equivalently, reject when

\[\barX_n < \frac{200}{2n}\,\chi^2_{2n,1-\alpha}\]

No data has been observed yet

Step 4: Observed Data

Let

\[n=10,\qquad \barx_n=176\]

Then \[t_{\text{obs}}=\frac{2(10)(176)}{200}=17.60\]

Step 5: \(p\)-value and decision

The \(p\)-value is

\[p=\Prob\big(\chi^2_{20} \le 17.60\big) \approx 0.39\]

Reject \(H_0\) iff \(p\le \alpha\)So we do NOT reject \(H_0\) at the \(\alpha=0.05\) level. This is not the same as accepting \(H_0\)!

Type I and Type II Errors

Type I error \(\alpha\):

Falsely conclude that reliability has worsened when the true mean time between failures is 200 hours \[\alpha=\Prob(\text{reject }H_0\mid \mu=200)\]

Type II error \(\beta(\mu_1)\) (for some \(\mu_1<200\)):

Fail to detect that the system is less reliable than claimed \[ \beta(\mu_1) = \Prob(\text{fail to reject }H_0 \mid \mu = \mu_1) \]

Power function \(\power(\mu_1)\)

The probability of correctly detecting reduced reliability (for some \(\mu_1<200\))

\[ \power(\mu_1) = \Prob(\text{reject }H_0 | \mu = \mu_1) = 1-\beta(\mu_1) \]

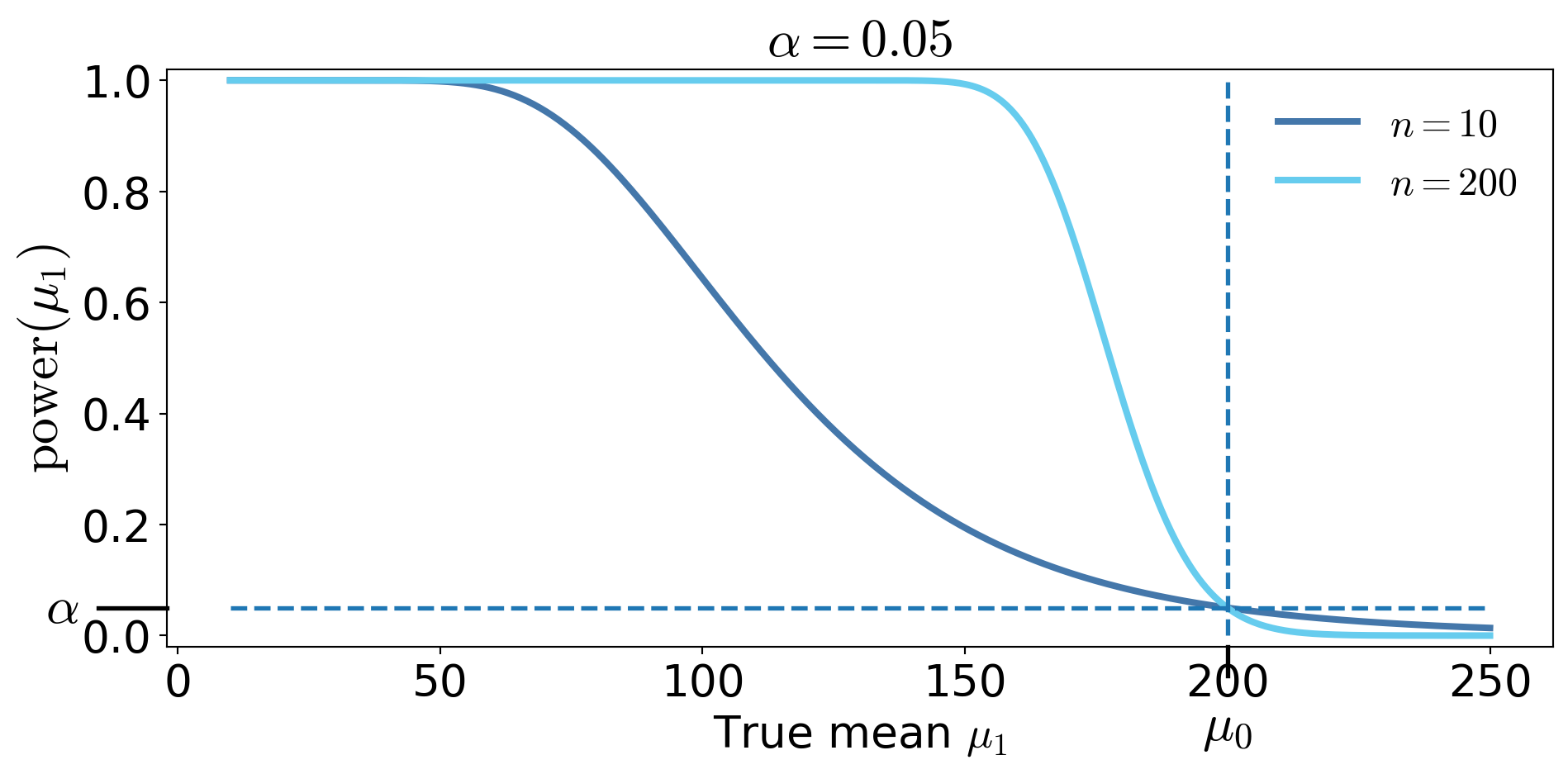

Power for the Server Reliability test

From Step 3, we reject \(H_0\) when

\[T(\boldsymbol{X})=\frac{2n\barX_n}{200} < \chi^2_{2n,1-\alpha}\]

If the true mean is actually \(\mu_1\), then \[\frac{200 T(\boldsymbol{X}) }{\mu_1} = \frac{2n\barX_n }{\mu_1} \sim\chi^2_{2n}\]

, the power function is \[\begin{align*} \power(\mu_1) &= \Prob\!\left(T(\boldsymbol{{X}}) < \chi^2_{2n,\,1-\alpha}\mid \mu=\mu_1\right) = \Prob\!\left(\frac{200\,T(\boldsymbol{X})}{\mu_1} \sim \chi^2_{2n} < \frac{200\,\chi^2_{2n,\,1-\alpha}}{\mu_1} \,\middle|\, \mu=\mu_1\right)\\ &\qquad \qquad \text{increases as $\mu_1$ decreases.} \end{align*}\]

Power Curves

Do not use the power curve to decide whether to reject after seeing the data

Power is about the test procedure, not about the observed data

Two kinds of error

\[\begin{gather*} H_0 \text{ null hypothesis (default, innocence) in terms of } \theta \\ H_A \text{ alternative hypothesis (evidence, guilt) in terms of } \theta \end{gather*}\]

\(H_0\) and \(H_A\) are mutually exclusive

Truth vs Decision

| Reject \(H_0\) | Do Not Reject \(H_0\) | |

|---|---|---|

| \(H_0\) true | Type I error probability \(\alpha\) |

Correct |

| \(H_0\) false | Correct probability \(\power(\theta)\) |

Type II error probability \(\beta(\theta)\) |

Confidence intervals & hypothesis testing

Structural comparison

| Confidence Interval | Hypothesis Test |

|---|---|

| An interval of plausible values | A reject / do not reject decision |

| Random interval | Random decision |

| Statement about \(\theta\) | Statement about \(H_0\) |

| No special value privileged | Tests a specific value \(\theta_0\) |

Shared ingredients

| Both Use | Meaning |

|---|---|

| Level \(\alpha\) | Willingness to be wrong |

| Pivot / test statistic | Standardized measure of evidence |

| Sampling distribution | Controls coverage / Type I error |

\[ \theta_0 \text{ rejected at level } \alpha \iff \theta_0 \notin \text{corresponding } (1-\alpha) \text{ confidence interval} \]

Hypothesis Testing: Design vs Data

%%{init: {"themeVariables":{"fontSize":"36px"}}}%%

flowchart LR

D1T["Design Phase<br/>(Before Data)"]

D2T["Data Phase<br/>(After Data)"]

subgraph D1 [ ]

A[Model<br/>Assumptions]

B[Choose Test<br/>Statistic]

C[Sampling<br/>Distribution<br/>under null]

D["Fix Rejection<br/>Region<br/>(size α)"]

end

subgraph D2 [ ]

E[Observe<br/>Data]

F[Compute<br/>Test<br/>Statistic]

G[Decision:<br/>Reject or Not]

end

D1T --> A

D2T --> E

A --> B --> C --> D --> E --> F --> G

style D1 fill:transparent,stroke:#888,stroke-width:2px

style D2 fill:transparent,stroke:#888,stroke-width:2px

style D1T fill:transparent,stroke:transparent,font-weight:bold

style D2T fill:transparent,stroke:transparent,font-weight:bold

Emphasis

Everything in the Design Phase defines the procedure

- \(\alpha\) and power belong to the Design Phase

The Data Phase only applies the pre-defined rule

The power curve describes the procedure, not the observed dataset

What depends on data and what does not?

Chosen before seeing data

| Quantity | Who chooses it? |

|---|---|

| \(H_0\) and \(H_A\) | Us |

| Form of test statistic \(T\) | Us |

| Significance level \(\alpha\) | Us |

| Sample size \(n\) | Us |

| Rejection region \(\RR\) | Determined by \(\alpha\) & \(n\) (once \(H_0\), \(T\) are fixed) |

| Type II error \(\beta(\theta)\) \(\power(\theta)\) |

Determined by \(\alpha\), \(n\), & \(\theta\) |

Once \(H_0\) and \(T\) are fixed:

- One may choose two of \(\alpha\), \(n\), and \(\RR\),

- But not all three independently

Depends on data

| Quantity | Why? |

|---|---|

| Test statistic value | Computed from sample |

| p-value | Function of statistic |

| Decision (reject / not reject) | Depends on statistic |

Forms of \(H_0\) and \(H_A\)

Common structures

| Type | \(H_0\) | \(H_A\) |

|---|---|---|

| Two-sided | \(\theta = \theta_0\) | \(\theta \ne \theta_0\) |

| One-sided (upper) | \(\theta = \theta_0\) | \(\theta > \theta_0\) |

| One-sided (lower) | \(\theta = \theta_0\) | \(\theta < \theta_0\) |

| Two simple values | \(\theta = \theta_0\) | \(\theta = \theta_1\) |

Simple: a single \(\theta\) value

Composite: multiple \(\theta\) values

Composite null example

| Version A | Version B | |

|---|---|---|

| \(H_0:\ \theta = \theta_0\) | \(H_0:\ \theta \ge \theta_0\) | Same? |

| \(H_A:\ \theta < \theta_0\) | \(H_A:\ \theta < \theta_0\) |

The test is calibrated at the boundary:

\[\begin{align*} \text{A}: \quad &\Prob(\text{Reject } H_0 \mid \theta_0)=\alpha \\ \text{B}: \quad &\sup_{\theta \ge \theta_0} \Prob(\text{Reject } H_0 \mid \theta) = \alpha \end{align*}\]

Key idea

- \(H_0\) may be composite

- The boundary value controls Type I error

- Test the least favorable value

Examples of hypothesis testing

(CB §8.1–8.3; WMS §10.3-10.9)

Building on the established framework

Translating words into \(H_0\) and \(H_A\)

- \(H_0\) contains the status quo — often written with equality

- \(H_A\) reflects the research claim

Examples

| Words | \(H_0\) | \(H_A\) |

|---|---|---|

| “Is the mean different from 10?” | \(\theta = 10\) | \(\theta \ne 10\) |

| “Is the mean greater than 10?” | \(\theta = 10\) | \(\theta > 10\) |

| “Is the defect rate below 5%?” | \(\theta = 0.05\) | \(\theta < 0.05\) |

| “Has the process changed?” | \(\theta = \theta_0\) | \(\theta \ne \theta_0\) |

| “Our average time between failures is greater than 200 hours” | \(\mu = 200\) | \(\mu > 200\) |

| “Your average time between failures is less than 200 hours” | \(\mu = 200\) | \(\mu < 200\) |

| “Our job placement rate is 90%, not 70%” (both simple) | \(p = 0.7\) | \(p = 0.9\) |

Definition of the \(p\)-value

The \(p\)-value is the probability, computed under \(H_0\), of observing a test statistic at least as extreme as the one observed, assuming \(H_0\) is true

If \(T\) is the test statistic and \(t_{\text{obs}}\) is the observed value, then

Right-tailed test: \(\quad p\text{-value} = \Prob_{H_0}(T \ge t_{\text{obs}})\)

Left-tailed test: \(\quad p\text{-value} = \Prob_{H_0}(T \le t_{\text{obs}})\)

Two-sided test: \(\quad p\text{-value} = \Prob_{H_0}(|T| \ge |t_{\text{obs}}|)\)

Compute \(p\)-values after setting the significance level \(\alpha\), rather than choosing \(\alpha\) after seeing the data

Changing \(\alpha\) after seeing the \(p\)-value is a form of data snooping

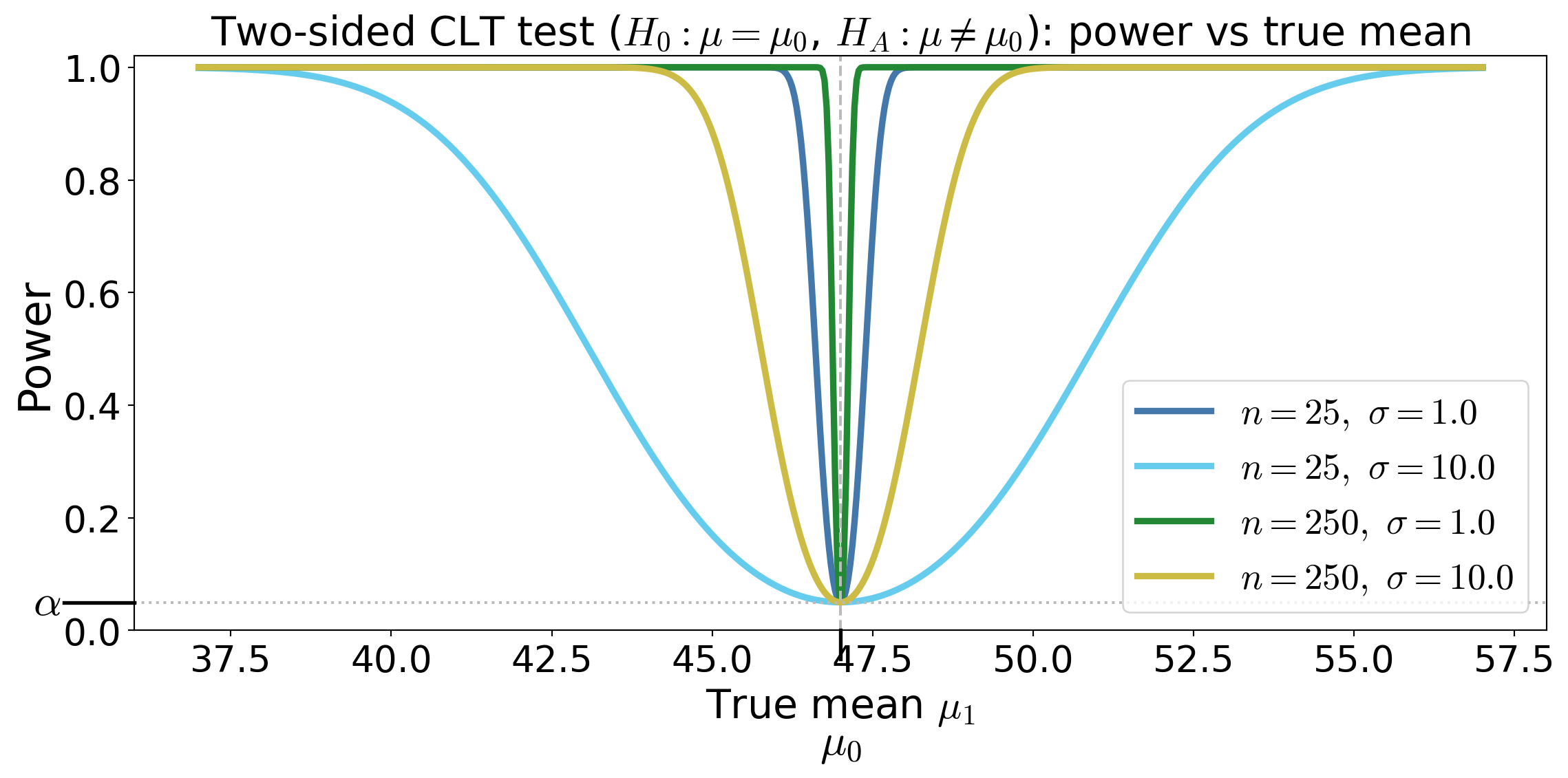

Two-sided CLT-enabled test for a mean assuming large sample size

Suppose \(X_1,\dots,X_n\) IID with \(\Ex(X_i) = \mu\), \(\var(X_i) = \sigma^2\) with large \(n\)

Test \(H_0: \mu = \mu_0\) against \(H_A: \mu \ne \mu_0\)

Test statistic \(\displaystyle Z_n(\vX) = \frac{\barX_n - \mu_0}{S_n/\sqrt{n}} \appxsim \Norm(0,1) \text{ for large } n \text{ under } H_0\)

Rejection region \(\RR = (-\infty, -z_{\alpha/2}) \cup (z_{\alpha/2}, \infty)\)

Power function — the probability of rejecting \(H_0\) when the true mean is \(\mu_1\)

- (approximate power, treating \(S_n\approx \sigma\) for large \(n\))

\[ \power(\mu_1)= \Prob(|Z_n(\vX)|>z_{\alpha/2} \mid \mu = \mu_1) = 1 - \Phi\!\left(z_{\alpha/2} - \frac{\mu_1-\mu_0}{\sigma/\sqrt{n}}\right) + \Phi\!\left(-z_{\alpha/2} - \frac{\mu_1-\mu_0}{\sigma/\sqrt{n}}\right ) \]

- \(p\)-value for observed \(z_{\text{obs}}\) is \(p = 2\big(1 - \Phi(|z_{\text{obs}}|)\big)\)

Power curves for the two-sided CLT test

Power is \(\Prob(\text{reject} \mid \theta)\)

It is not \(\Prob(\theta \mid \text{data})\)

Power describes the test design, not the evidence in this sample

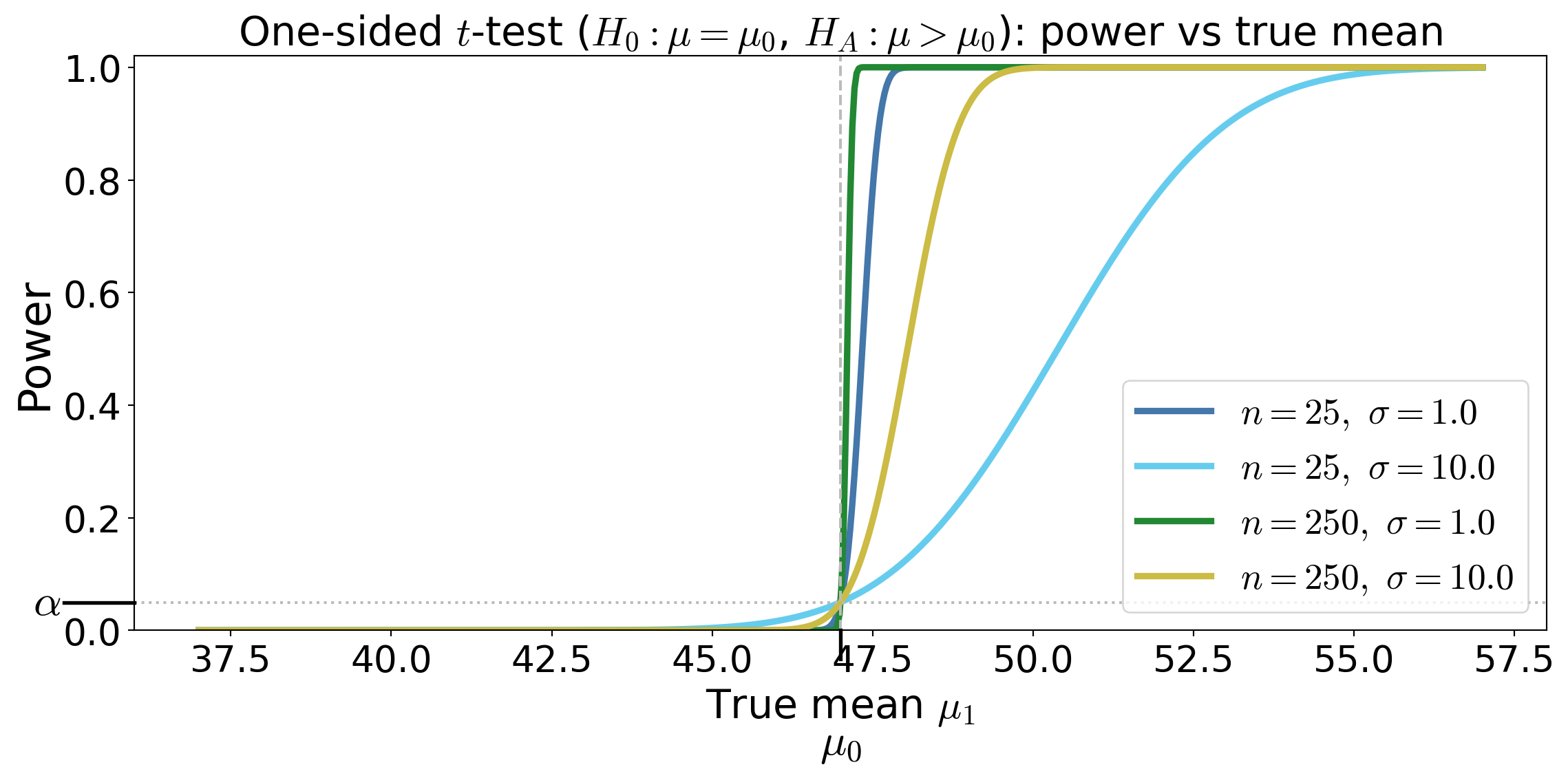

One-sided test for a mean under Normal data

Suppose \(X_1,\dots,X_n\) IID with \(X_i \sim \Norm(\mu,\sigma^2)\)

Test \(H_0: \mu \le \mu_0\) against \(H_A: \mu > \mu_0\)

Test statistic \(\displaystyle T_n(\vX) = \frac{\barX_n - \mu_0}{S_n/\sqrt{n}} \sim t_{n-1} \text{ under } \mu=\mu_0\)

Rejection region \(\RR = (t_{n-1,\alpha}, \infty)\)

Power function — the probability of rejecting \(H_0\) when the true mean is \(\mu_1\)

\[\begin{multline*} T_n(\vX) \sim t_{n-1}(\delta) \text{ for } \delta = \frac{\mu_1 - \mu_0}{\sigma/\sqrt{n}} \\ \implies \power(\mu_1) = \Prob(T_n(\vX) > t_{n-1,\alpha} \mid \mu=\mu_1) = 1 - F_{t_{n-1}(\delta)}\!\left(t_{n-1,\alpha}\right) \end{multline*}\]

where \(F_{t_{n-1}(\delta)}\) is the CDF of the noncentral t distribution with \(n-1\) degrees of freedom and noncentrality parameter \(\delta\)

- \(p\)-value for observed \(t_{\text{obs}}\) is \(p = \Prob(t_{n-1} \ge t_{\text{obs}})\)

Power curves for the one-sided \(t\)-test

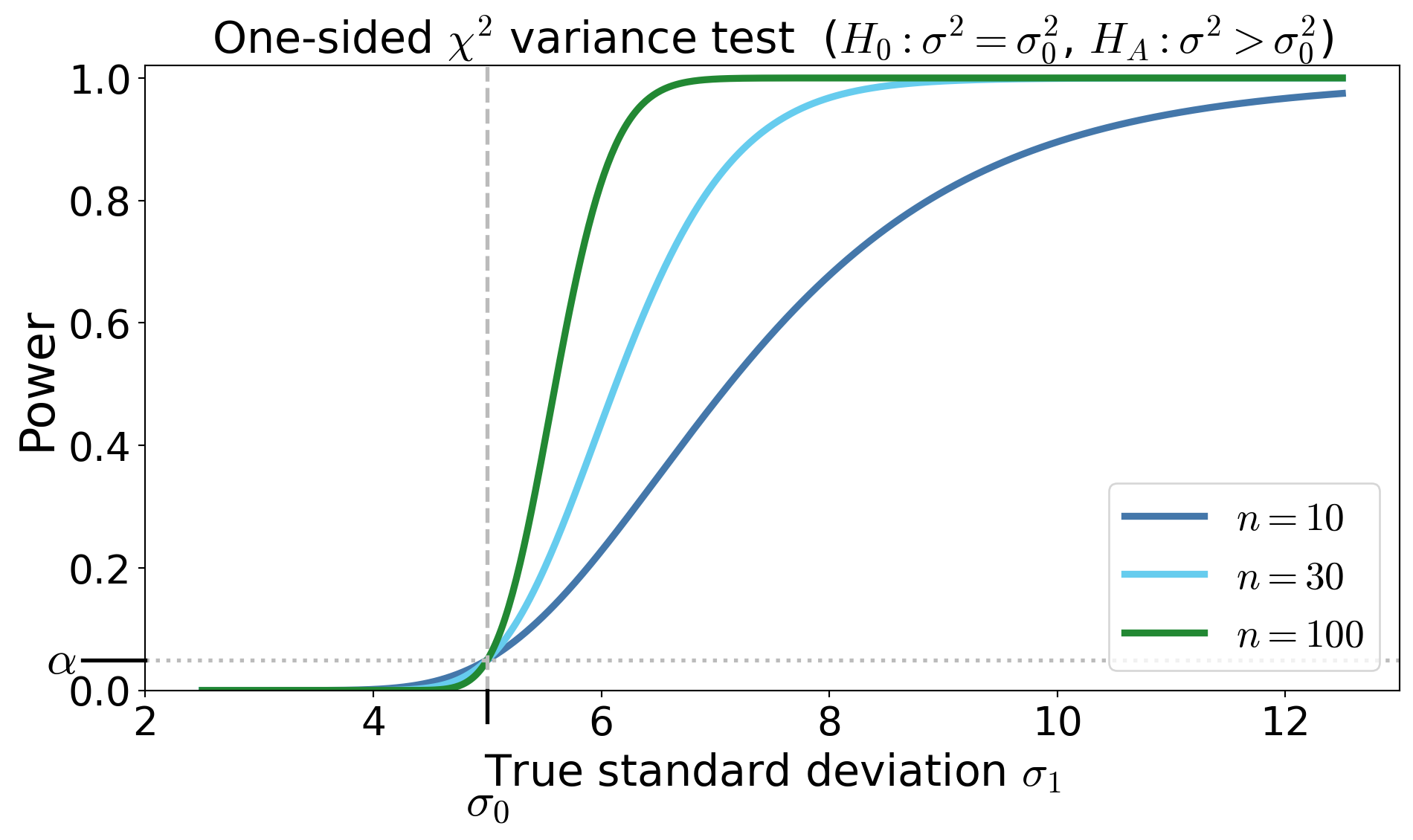

One-sided \(\chi^2\) test for the variance under Normal data

Suppose \(X_1,\dots,X_n\) IID with \(X_i \sim \Norm(\mu,\sigma^2)\).

Test \(H_0: \sigma^2 = \sigma_0^2\) against \(H_A: \sigma^2 > \sigma_0^2\)

Pivot / test statistic \(\displaystyle T_n(\vX) = \frac{(n-1)S_n^2}{\sigma_0^2} \sim \chi^2_{n-1} \text{ under } H_0\)

- where \(S_n^2\) is the unbiased sample variance

Rejection region \(\RR = (\chi^2_{n-1,\alpha}, \infty)\)

Power function

\[ \power(\sigma_1) = \Prob\!\left( T_n(\vX) > \chi^2_{n-1,\alpha}\mid \sigma = \sigma_1 \right) = \Prob\!\left( \chi^2_{n-1} > \frac{\sigma_0^2}{\sigma_1^2}\chi^2_{n-1,\alpha} \right) \]\(p\)-value for observed \(t_{\text{obs}}\) is \(p = \Prob(\chi^2_{n-1} \ge t_{\text{obs}})\)

Power curves for the one-sided \(\chi^2\) test

Try on your own

\(\exstar\)Construct small sample size one-sided and two-sided tests for the mean of an exponential distribution and sketch the power curves

Optimal Tests and Likelihood Methods

(CB §8.2–8.3; WMS §10.10-10.11)

From procedures to optimality

We have constructed tests, and we have computed their size and power, but

Among all tests with size \(\alpha\), which test has the highest power against a fixed alternative?

To compare two hypotheses

\[ H_0: \theta = \theta_0 \qquad \text{vs} \qquad H_A: \theta = \theta_A \]

Consider the likelihood ratio statistic constructed from the ratio of the likelihood values based on data \(\vX = (X_1,\dots,X_n)\): \[ \Lambda(\vX) = \frac{L(\theta_0 \mid \vX)} {L(\theta_A \mid \vX)} = \frac{\varrho_{\vX}(\vX \mid \theta_0)}{\varrho_{\vX}(\vX \mid \theta_A)} \]

If the data are much more likely under \(H_A\) than under \(H_0\), the ratio \(\Lambda(\vX)\) will be small, and this is evidence against \(H_0\)

Neyman–Pearson lemma (simple vs simple)

Test

\[ H_0:\theta=\theta_0 \qquad\text{vs}\qquad H_A:\theta=\theta_A \]

Among all tests with size \(\alpha\), the test that rejects for sufficiently small likelihood ratio is most powerful

Reject \(H_0\) when

\[ \Lambda(\vX) = \frac{L(\theta_0 \mid \vX)} {L(\theta_A \mid \vX)} < k \]

where \(k\) is chosen so that

\[ \Prob(\text{reject }H_0 \mid \theta = \theta_0)= \Prob(\Lambda(\vX) < k \mid \theta = \theta_0) = \alpha \]

A test that is most powerful for all alternatives in a class is called uniformly most powerful (UMP)

Example: mean of IID Normal data with known \(\sigma\), testing simple vs simple

\[ H_0:\mu=\mu_0 \qquad H_A:\mu=\mu_A \quad \text{with } \mu_A > \mu_0 \]

Suppose \(X_1,\dots,X_n \IIDsim \Norm(\mu,\sigma^2)\). The likelihood ratio test statistic based on this data, \(\vX = (X_1,\dots,X_n)\), is

\[ \Lambda = \frac{L(\mu_0 \mid \vX)}{L(\mu_A \mid \vX)} \]

Because the logarithm is increasing, it is convenient to work with

\[\begin{multline*} \log \Lambda(\vX) = \log \bigl(L(\mu_0 \mid \vX)\bigr)-\log L(\mu_A \mid \vX) \\ = -\frac{1}{2\sigma^2} \sum_{i=1}^n (X_i-\mu_0)^2 + \frac{1}{2\sigma^2} \sum_{i=1}^n (X_i-\mu_A)^2 = \cdots \\ = \frac{n(\mu_0-\mu_A)}{\sigma^2} \left(\barX_n - \frac{\mu_0+\mu_A}{2}\right) \end{multline*}\]

\[\begin{equation*} \log \Lambda(\vX) = \frac{n(\mu_0-\mu_A)}{\sigma^2} \left(\barX_n - \frac{\mu_0+\mu_A}{2}\right) \end{equation*}\]

Reject when \(\barX_n > c\) for some cut-off \(c\), which is chosen so that

\[ \Prob(\barX_n>c \mid \mu=\mu_0)=\alpha, \qquad \text{i.e., } c = \mu_0 + z_\alpha \frac{\sigma}{\sqrt n} \]

Because the Type-I error is computed assuming \(H_0\) is true, the cutoff does not depend on \(\mu_A\)

The likelihood ratio test is most powerful among all tests with size \(\alpha\) for testing \(H_0: \mu = \mu_0\) vs \(H_A: \mu = \mu_A\) with \(\mu_A > \mu_0\) when \(\sigma\) is known

The likelihood ratio test therefore reproduces the classical \(z\)-test for the mean of a normal distribution with known variance

From Neyman–Pearson to likelihood ratio tests for composite hypotheses

More generally, for hypotheses

\[ H_0:\theta \in \ct_0 \qquad\text{vs}\qquad H_A:\theta \in \ct_A \]

the likelihood ratio statistic based on data \(\vX = (X_1,\dots,X_n)\) is

\[ \Lambda(\vX) = \frac{\sup_{\theta\in \ct_0} L(\theta \mid \vX)} {\sup_{\theta\in \ct} L(\theta \mid \vX)} =\frac{\text{best fit under }H_0} {\text{best fit over the entire parameter space}} \]

- The numerator is the largest likelihood under \(H_0\)

- The denominator is the largest likelihood over the entire parameter space

Reject for small \(\Lambda\)

Example: mean of IID Normal data with known \(\sigma\), testing simple vs composite (two-sided)

\[ H_0:\mu=\mu_0 \qquad H_A:\mu\ne \mu_0 \]

Suppose \(X_1,\dots,X_n \IIDsim \Norm(\mu,\sigma^2)\). The likelihood ratio test statistic is

\[ \Lambda(\vX) = \frac{\sup_{\mu=\mu_0} L(\mu \mid \vX)} {\sup_{\mu\in\reals} L(\mu \mid \vX)} = \frac{L(\mu_0 \mid \vX)}{L(\barX_n \mid \vX)}, \qquad \text{since the MLE of $\mu$ is $\barX_n$ for IID normal data} \]

Because the logarithm is increasing, it is convenient to work with

\[\begin{multline*} \log \Lambda(\vX) = \log L(\mu_0 \mid \vX)-\log L(\barX_n \mid \vX) \\ = -\frac{1}{2\sigma^2}\sum_{i=1}^n (X_i-\mu_0)^2 +\frac{1}{2\sigma^2}\sum_{i=1}^n (X_i-\barX_n)^2 = \cdots = -\frac{n}{2\sigma^2}(\barX_n-\mu_0)^2 \end{multline*}\]

\[\begin{equation*} \log \Lambda(\vX) = -\frac{n}{2\sigma^2}(\barX_n-\mu_0)^2 \end{equation*}\]

Reject when \(\Lambda(\vX)\) is small \(\iff |\barX_n-\mu_0|\) is large, equivalently, reject when

\[ \left|\frac{\barX_n-\mu_0}{\sigma/\sqrt n}\right| > z_{\alpha/2} \]

The cutoff is chosen so that

\[ \Prob\!\left(\left|\frac{\barX_n-\mu_0}{\sigma/\sqrt n}\right|>z_{\alpha/2}\ \middle|\ \mu=\mu_0\right)=\alpha, \]

which depends only on \(\mu_0\), \(\sigma\), \(n\), and \(\alpha\)

The likelihood ratio test therefore reproduces the classical two-sided \(z\)-test for the mean of a normal distribution with known variance

Example: LRT for a normal mean (unknown variance) — nuisance parameters

\[ H_0:\mu=\mu_0 \qquad \text{vs} \qquad H_A:\mu\ne\mu_0 \]

Suppose \(X_1,\dots,X_n \IIDsim \Norm(\mu,\sigma^2)\)

Parameter vector: \(\theta=(\mu,\sigma^2), \qquad \sigma^2\) is a nuisance parameter

Step 1: Unrestricted MLE

Log-likelihood: \[ \ell(\mu,\sigma^2) = -\frac{n}{2}\log (\sigma^2) - \frac{1}{2\sigma^2} \sum_{i=1}^n (X_i-\mu)^2 + \text{constants} \]

Maximizing gives \[\begin{gather*} \mu_{\MLE} = \barX_n, \qquad \sigma_{\MLE}^2 = \frac{1}{n}\sum_{i=1}^n (X_i-\barX_n)^2 = \frac{n-1}{n} S_n^2 \\ \sup_{\mu,\sigma^2} \ell(\mu,\sigma^2) = -\frac{n}{2}\log (\sigma^2_{\MLE}) - \frac{n}{2} + \text{constants} \end{gather*}\]

Step 2: MLE under \(H_0\)

Under \(\mu=\mu_0\), \[\begin{gather*} \sigma_{0,\MLE}^2 = \frac{1}{n}\sum_{i=1}^n (X_i-\mu_0)^2 = (\barX_n - \mu_0)^2 + \frac 1n \sum_{i=1}^n (X_i-\barX_n)^2 = (\barX_n - \mu_0)^2 + \sigma_{\MLE}^2 \\ \sup_{\sigma^2} \ell(\mu_0,\sigma^2) = -\frac{n}{2}\log (\sigma^2_{0,\MLE}) - \frac{n}{2} + \text{constants} \end{gather*}\]

Step 3: (Log) likelihood ratio

\[\begin{gather*} \log \bigl(\Lambda(\vX) \bigr) = \sup_{\sigma^2} \ell(\mu_0,\sigma^2_{0,\MLE}) - \sup_{\mu,\sigma^2} \ell(\mu,\sigma^2_{\MLE}) = -\frac{n}{2}\log (\sigma^2_{0,\MLE}) + \frac{n}{2}\log (\sigma^2_{\MLE}) \\ \Lambda(\vX) = \left(\frac{\sigma^2_{0,\MLE}}{\sigma^2_{\MLE}}\right)^{-n/2} \end{gather*}\]

Step 4: Where nuisance disappears

Therefore \[\begin{align*} \frac{\sigma_{0,\MLE}^2}{\sigma_{\MLE}^2} & = \frac{(\barX_n - \mu_0)^2 + \sigma_{\MLE}^2}{\sigma_{\MLE}^2} = \frac{(\barX_n-\mu_0)^2} {(n-1) S_n^2/n} + 1 = \frac{T_n^2}{n-1} + 1\\ \Lambda(\vX) & = \left( 1 + \frac{T_n^2}{n-1} \right)^{-n/2} \end{align*}\]

where \(\displaystyle T_n = \frac{\barX_n-\mu_0}{S/\sqrt n}\) is the familiar \(t\)-statistic

The likelihood ratio depends only on the \(t\)-statistic for testing \(H_0: \mu = \mu_0\) vs \(H_A: \mu \ne \mu_0\)

The nuisance parameter \(\sigma^2\) has disappeared

\(\exstar\) Show that the LRT for testing \(H_0: \mu = \mu_0\) vs \(H_A: \mu = \mu_1\) with \(\mu_1 > \mu_0\) and \(\sigma\) unknown is the familar one-sided \(t\)-test as

Wilks’ Theorem

\[ \Lambda(\vX) = \frac{\displaystyle \sup_{\theta\in \ct_0} L(\theta \mid \vX)} {\displaystyle \sup_{\theta\in \ct} L(\theta \mid \vX)} \]

Under regularity conditions,

\[ -2 \log \Lambda \dto \chi^2_{\df} \] where the degrees of freedom is \[ \df = \dim(\text{full model}) - \dim(\text{null model}) \]

Example: Normal data with unknown \(\sigma\)

- Full model for \(\Norm(\mu,\sigma^2)\) has \(\dim(\ct) = 2\)

- Null model for \(H_0: \mu = \mu_0\) has \(\dim(\ct_0) = 1\)

- \(\df = 2 - 1 = 1\)

Why bother with the likelihood ratio test (LRT)

\[ \Lambda(\vX) = \frac{\sup_{\theta \in \ct_0} L(\theta \mid \vX)} {\sup_{\theta \in \ct} L(\theta \mid \vX)} \qquad \text{Reject when $\Lambda(\vX)$ is small} \]

Even though

We already know the \(z\), \(t\), and other tests

We still need to choose the rejection region cut-off to get the desired size \(\alpha\)

However, the LRT

Is a unifying concept

Handles composite hypotheses

Reproduces \(z\), \(t\), \(\chi^2\), \(F\) tests

Scales to multi-parameter models

Has large-sample theory (Wilks)

\(\exstar\) WMS 10.105, 10.106, 10.112

\(\exstar\) CB 8.29, 8.40, 8.41

Proof of the Neyman–Pearson lemma (simple vs simple)

\[ H_0:\theta=\theta_0, \qquad H_A:\theta=\theta_1 \]

Let the joint densities of \(\vX\) under \(\theta_0\) and \(\theta_1\) be \(\varrho_0(\vx)\) and \(\varrho_1(\vx)\).

Among all tests with size \(\alpha\), the likelihood ratio test is most powerful.

Given data \(\vX\), reject \(H_0\) when \[ \Lambda(\vx) = \frac{L(\theta_0\mid \vx)}{L(\theta_1\mid \vx)} = \frac{\varrho_0(\vx)}{\varrho_1(\vx)} < k, \qquad\text{i.e.}\qquad \varrho_0(\vx)-k\varrho_1(\vx)<0 \] where \(k\) is chosen so that \[ \Prob(\text{Reject }H_0\mid \theta=\theta_0)=\alpha \]

Proof by comparison argument

For convenience of notation, we defined rejection regions in terms of data, \(\vX\), rather than test statistics. Let the likelihood ratio test have rejection region: \[ \RR^{\LRT}=\{\vX:\ \varrho_0(\vX)-k\varrho_1(\vX)<0\} \] Thus it rejects with indicator \(\indic(\vX\in \RR^{\LRT})\)

Let \(T(\vX)\) be any other test statistic with rejection region \(\RR\) (for data \(\vX\))

Assume this competing test has size at most \(\alpha\):

\[\begin{multline*} \int \indic(\vx\in\RR)\,\varrho_0(\vx)\,\dif\vx = \Ex [ \indic(\vX\in\RR) \mid \theta=\theta_0] = \Prob(\vX\in\RR\mid \theta=\theta_0) \\ \le \alpha = \Prob(\vX\in\RR^{\LRT}\mid \theta=\theta_0) = \Ex [ \indic(\vX\in\RR^{\LRT}) \mid \theta=\theta_0] = \int \indic(\vx\in\RR^{\LRT})\,\varrho_0(\vx)\,\dif\vx \end{multline*}\]

Consider the integral \[ I = \int \underbrace{\bigl[\indic(\vx\in\RR^{\LRT})-\indic(\vx\in\RR)\bigr]}_{\text{which test is rejecting?}} \underbrace{\bigl[\varrho_0(\vx)-k\varrho_1(\vx)\bigr]}_{\LRT \text{ will reject if this is negative}}\,\dif\vx \]

Step 1: \(I\le 0\)

Check pointwise signs:

If \(\vx\in\RR^{\LRT}\) but \(\vx\notin\RR\), then \(\indic(\vx\in\RR^{\LRT})-\indic(\vx\in\RR)=1\) and \(\varrho_0(\vx)-k\varrho_1(\vx) < 0\), so the product is \(\le 0\)

If \(\vx\notin\RR^{\LRT}\) but \(\vx\in\RR\), then \(\indic(\vx\in\RR^{\LRT})-\indic(\vx\in\RR)=-1\) and \(\varrho_0(\vx)-k\varrho_1(\vx) \ge 0\), so the product is also \(\ge 0\)

Otherwise the difference of indicators is \(0\).

Hence the integrand is everywhere \(\le 0\), so \(I\le 0\)

Step 2: Expand \(I\) and use the size constraint

Expand: \[\begin{multline*} I = \int\bigl[\indic(\vx\in\RR^{\LRT})-\indic(\vx\in\RR)\bigr]\varrho_0(\vx)\,\dif\vx \\ - k\int\bigl[\indic(\vx\in\RR^{\LRT})-\indic(\vx\in\RR)\bigr]\varrho_1(\vx)\,\dif\vx \le 0 \end{multline*}\]

The size condition implies \[\begin{multline*} \int\bigl[\indic(\vx\in\RR^{\LRT})-\indic(\vx\in\RR)\bigr]\varrho_0(\vx)\,\dif\vx \\ = \Prob(\vX\in\RR^{\LRT}\mid \theta=\theta_0)-\Prob(\vX\in\RR\mid \theta=\theta_0) = \alpha - \Prob(\vX\in\RR\mid \theta=\theta_0) \ge 0 \end{multline*}\]

Therefore, since \(I\le 0\), \[ k\int\bigl[\indic(\vx\in\RR^{\LRT})-\indic(\vx\in\RR)\bigr]\varrho_1(\vx)\,\dif\vx \ge \int\bigl[\indic(\vx\in\RR^{\LRT})-\indic(\vx\in\RR)\bigr]\varrho_0(\vx)\,\dif\vx \ge 0, \]

Because \(k>0\), we have \[ \int\bigl[\indic(\vx\in\RR^{\LRT})-\indic(\vx\in\RR)\bigr]\varrho_1(\vx)\,\dif\vx \ge 0 \]

That is, \[\begin{multline*} \power^{\LRT}(\theta_1) = \Prob(\vX \in \RR^{\LRT} \mid \theta=\theta_1) = \int \indic(\vx\in\RR^{\LRT})\,\varrho_1(\vx)\,\dif\vx \\ \ge \int \indic(\vx\in\RR)\,\varrho_1(\vx)\,\dif\vx = \Prob(\vX \in \RR \mid \theta=\theta_1)= \power(\theta_1) \end{multline*}\]

Therefore \(\power^{\LRT}(\theta_1)\ge \power(\theta_1)\) for every test with size at most \(\alpha\) so the likelihood ratio test is most powerful

\(\square\)

© 2026 Fred J. Hickernell · Illinois Tech · assisted by ChatGPT · Hypothesis Testing · MATH 563 — Mathematical Statistics Website · \(\exstar\) = exercise